In my world, it seems there are two types of business plans:

- Plan #1 has the obligatory 3-5 year annual financials, so the "numbers" box has been checked.

- Plan #2 is backed by a detailed, dynamic, well-thought-through financial model. It has the obligatory financials page, but shows the details in the addendum.

Plan #2 has a massive advantage over plan #1 because it really shows the founders have done their homework. They have taken all the product, market, sales channel, peer and competitor information and driven it down into a detailed, executable roadmap of how the product gets to market.

Once you go through the process of building a detailed financial model, you'll be able to answer the following questions:

Why are you asking for this particular amount of funding (good example of a successful answer here)? Exactly how far will your cash take you? Do you have enough cash to get you to the next major valuation milestone?

What exactly will you spend your cash on? Headcount vs. capital expenditures vs. outsourced consulting vs. marketing, licensing, etc...

Who are your key hires over the next year? When will they be brought on?

What are the details behind the revenue assumptions? Have you thought through the difference between revenue and cash receipts? What

When does the business begin to scale? Once you begin to scale, how does your business compare to your competitors, your peers? Are your key metrics in line? Are you being realistic on your scaling assumptions?

What public company are you modeling yourself after? How does their growth and financing scenario compare to yours? Are your valuation assumptions reasonable?

Have you done sensitivity analysis? What are your downside scenarios, and what actions do you take - and when will you take them - if you find yourself in one of these scenario? At any given point along the road, how would you circle the wagons and conserve cash?

Building a successful new business has a lot to do with focus and managing uncertainty. If you take the time necessary to really build out a great financial model, you will have gone a long way toward increasing your focus and managing the uncertainty. And your potential/existing investors will definitely notice.

Brian Royston

Royston Financial Consulting, Inc.

Thursday, September 2, 2010

Sunday, July 25, 2010

Why is it important to spend time developing a well-thought-out financial model?

I dropped by a client's office last week to check in on him and see how the company was progressing. The founders and I built a detailed financial model for their company late last year. Early this year they were successful in raising a series A round of $5M.

He had told me earlier that the potential investors were impressed with the model, but last week he told me how key that model was in the process. He said, "Did I tell you that the model got us an extra million dollars?" I didn't recall him telling me this, so I asked him to explain. He said that he had received a couple of term sheets for $4M in funding. He really wanted $5M, so he pulled the model out and said, "We really need $5M, and here's why." He took them through the model and explained in great detail what expenditures were needed to get them to the next major milestone. They ended up getting the $5M!

That is a great example of the benefit of taking the time to build out a realistic, detailed, well-thought-out financial model. My client took financial modeling seriously...because he took his company seriously. After I built the basic structure of the model, we spent several sessions where we populated it with assumptions and refined it. We attacked the assumptions from different angles and finally arrived at a model they thought was aggressive, realistic and defend-able.

When you've done a deep dive with a financial model, you understand where the inflection points are, where the trade-offs are, what the key metrics are. You have a tangible set of expectations as the company moves forward. Most importantly, all of this knowledge comes across to your investors as a much deeper understanding of the business and how to execute the next phase.

By the way, he also said that he's nailed the model so far (from an expense standpoint), and that has given him loads of credibility with his investors. In the board meetings, they're not worried at all about cash, because the company is executing per the plan. This allows the meetings to focus on other important issues.

What was that extra $1M in funding worth? That's hard to quantify, but I'm sure my client would tell you that it was definitely worth the cost of the model!

Cheers,

B

He had told me earlier that the potential investors were impressed with the model, but last week he told me how key that model was in the process. He said, "Did I tell you that the model got us an extra million dollars?" I didn't recall him telling me this, so I asked him to explain. He said that he had received a couple of term sheets for $4M in funding. He really wanted $5M, so he pulled the model out and said, "We really need $5M, and here's why." He took them through the model and explained in great detail what expenditures were needed to get them to the next major milestone. They ended up getting the $5M!

That is a great example of the benefit of taking the time to build out a realistic, detailed, well-thought-out financial model. My client took financial modeling seriously...because he took his company seriously. After I built the basic structure of the model, we spent several sessions where we populated it with assumptions and refined it. We attacked the assumptions from different angles and finally arrived at a model they thought was aggressive, realistic and defend-able.

When you've done a deep dive with a financial model, you understand where the inflection points are, where the trade-offs are, what the key metrics are. You have a tangible set of expectations as the company moves forward. Most importantly, all of this knowledge comes across to your investors as a much deeper understanding of the business and how to execute the next phase.

By the way, he also said that he's nailed the model so far (from an expense standpoint), and that has given him loads of credibility with his investors. In the board meetings, they're not worried at all about cash, because the company is executing per the plan. This allows the meetings to focus on other important issues.

What was that extra $1M in funding worth? That's hard to quantify, but I'm sure my client would tell you that it was definitely worth the cost of the model!

Cheers,

B

Tuesday, July 13, 2010

Residential property investing – it’s all about the fundamentals

Back in 2002 I was looking for a good real estate-related investment. I live in the San Francisco Bay area, and was trying to find something close to home.

I wanted a long-term investment with a strong cashflow and limited downside potential. Being a finance guy, I schooled myself in the key metrics surrounding real estate investments (mainly capitalization rates and the relationship between rental rates and purchase price). I built a financial model that helped me to understand the fundamental parameters I was looking for. I looked at all types of properties: commercial, industrial, hospitality and residential…even assisted living facilities. I decided to focus on the residential market because I felt I understood it best, but it seemed I was chasing valuations up and up, and I couldn’t find anything that felt like a good value for the price.

I quickly came to the realization that, from a macro perspective, this was a really bad time to invest in real estate. All the money was moving out of the stock market into real estate, driving the prices up and the capitalization rates (and return on investment) down. California’s central valley was on fire…Sacramento housing prices were shooting up, and one-by-one, prices in the smaller towns in the central valley were rocketing up. I had to look outside California. Similar things were happening in Las Vegas, Phoenix, and other parts of the country. Everything I looked at was outside the parameters of my investment model. Everything seemed overvalued from a fundamental standpoint, and it seemed that everyone was playing a game of musical chairs hoping to get in and get out before the music stopped.

Either I needed to drop the idea or look for an area of the country that still had strong fundamentals. That’s when I started looking at East Texas. I found a great little town where I could find homes for $40K-$70K that would rent for $600-1,000 per month. This was over four times the rental rate per dollar invested than some of the other areas I was looking at. This fit my model, because even if I borrowed 100%, I could cashflow very well! Great fundamentals.

I next looked at the fundamentals of the town and surrounding area. I was very comfortable with the fundamentals of the area after I found the following:

I was 2,000 miles away, but if the numbers bore out the way my model projected, I could build a portfolio of rental homes that could support a management infrastructure, service the interest, principal and expenses, and still have a profit. It wasn’t sexy, and it wasn’t a get rich quick scheme…it was a good fundamental investment.

Besides, any appreciation on the homes would be gravy! Assuming a 5% annual growth in median home price over 20 years (the average growth in the area since 1970), the investment would be an 80% cash-on-cash capital gain. Better yet, if I financed 80% of the purchase, the return on investment would be over 800%!

Many of the residential home investment proposals I have seen over the past years had to make much, much more aggressive assumptions to achieve a strong return. The key assumption in their models, for instance, on an investment proposal for a home in California, Nevada or Arizona, was that median home values were going to increase at an annual rate of 15%+! This was fundamentally unattainable…it is 3X the historical appreciation of homes in the US. Other major assumptions in these models are 20+% down, the use of a negative amortization loan, and rapidly climbing rental rates…all very aggressive, risky assumptions. As the economics of the past few years have borne out, this was a massively faulty model, relying on pie-in-the-sky fundamental assumptions.

I decided to move forward with the East Texas investment model. We bought our first house in March, 2003, and quickly built up a portfolio of 50 properties, mostly single family homes and a couple of duplexes. The total amount of rentals is 60. We established local banking relationships and negotiated portfolio loans that would lend to our limited partnership. We have an internal staff that manages and maintains the properties, and the cashflow from the properties more than covers all our expenses and the paydown on the principal.

It was interesting to go through the housing crisis with this portfolio, because this is where the initial fundamentals of the model were put to their test. As it turns out, because the fundamental values of the homes were not out-of-whack to begin with, the median home prices remained steady throughout the housing crisis. The community continues to grow, and rental rates and occupancy continue to be strong.

As a side note, we weren’t fully scaled up around our property management and maintenance infrastructure because I felt that I wanted our internal costs to be less than if we hired an outside property management company. It was a couple of years ago, and I didn’t want to add to the portfolio because of the massive instability in the housing market and the fact that many of the banks were scared to lend. We looked at our capabilities and decided to start a heating and air conditioning company in the area, leveraging off the infrastructure we built to manage and maintain the property portfolio. The HVAC company is doing very well with minimal management focus, thanks to an interesting business model that is very different than the other related companies in the area. This has been an exciting venture which has increased the profit of our property portfolio because of the shared overhead costs. Now we’re fully scaled over our infrastructure.

I look back on the bullet I dodged by not investing with the crowd, and I feel very fortunate that I stuck with the fundamental principals upon which I started.

My major takeaways from this experience are 1) you can find a good investment even during a bad time to invest, 2) build a good conservative financial model, and; 3) ALWAYS stick to the fundamentals!

I’d love to hear other lessons learned while riding out the real estate crisis…

Cheers,

Brian Royston

Royston Financial Consulting, Inc.

I wanted a long-term investment with a strong cashflow and limited downside potential. Being a finance guy, I schooled myself in the key metrics surrounding real estate investments (mainly capitalization rates and the relationship between rental rates and purchase price). I built a financial model that helped me to understand the fundamental parameters I was looking for. I looked at all types of properties: commercial, industrial, hospitality and residential…even assisted living facilities. I decided to focus on the residential market because I felt I understood it best, but it seemed I was chasing valuations up and up, and I couldn’t find anything that felt like a good value for the price.

I quickly came to the realization that, from a macro perspective, this was a really bad time to invest in real estate. All the money was moving out of the stock market into real estate, driving the prices up and the capitalization rates (and return on investment) down. California’s central valley was on fire…Sacramento housing prices were shooting up, and one-by-one, prices in the smaller towns in the central valley were rocketing up. I had to look outside California. Similar things were happening in Las Vegas, Phoenix, and other parts of the country. Everything I looked at was outside the parameters of my investment model. Everything seemed overvalued from a fundamental standpoint, and it seemed that everyone was playing a game of musical chairs hoping to get in and get out before the music stopped.

Either I needed to drop the idea or look for an area of the country that still had strong fundamentals. That’s when I started looking at East Texas. I found a great little town where I could find homes for $40K-$70K that would rent for $600-1,000 per month. This was over four times the rental rate per dollar invested than some of the other areas I was looking at. This fit my model, because even if I borrowed 100%, I could cashflow very well! Great fundamentals.

I next looked at the fundamentals of the town and surrounding area. I was very comfortable with the fundamentals of the area after I found the following:

- Great infrastructure: although it was a small town (30-35K population), the big box retailers (Target, Home Depot, Big Lots, JC Penney, Blockbuster, Sam’s Club, etc) had already established themselves. The flagship hospitality infrastructure (Courtyard Marriot, Comfort Suites, Holiday Inn Express, Best Western, Hampton Inn, etc) had also come in and established themselves ahead of the curve. The education infrastructure was strong, with a great community college and a 10K+ student university within 30 minutes. The medical infrastructure was very strong and growing, with two major hospitals and outstanding medical services for seniors/retirees.

- Great location: the town was only a 90 minute drive from Houston International Airport, and close to all the amenities that a large city like Houston offers. It is flanked by two national forests and has two large reservoirs nearby.

- Vibrant, growing community: it is the county seat and retail hub of the area, so even though it has a population of 30-35K, it services a county population of over 80K. It has a low cost of living versus the national average, and it was ranked #1 in Texas as the strongest economy among micropolitan statistical areas.

- Median home valuations in the area had risen steadily and consistently since 1970.

I was 2,000 miles away, but if the numbers bore out the way my model projected, I could build a portfolio of rental homes that could support a management infrastructure, service the interest, principal and expenses, and still have a profit. It wasn’t sexy, and it wasn’t a get rich quick scheme…it was a good fundamental investment.

Besides, any appreciation on the homes would be gravy! Assuming a 5% annual growth in median home price over 20 years (the average growth in the area since 1970), the investment would be an 80% cash-on-cash capital gain. Better yet, if I financed 80% of the purchase, the return on investment would be over 800%!

Many of the residential home investment proposals I have seen over the past years had to make much, much more aggressive assumptions to achieve a strong return. The key assumption in their models, for instance, on an investment proposal for a home in California, Nevada or Arizona, was that median home values were going to increase at an annual rate of 15%+! This was fundamentally unattainable…it is 3X the historical appreciation of homes in the US. Other major assumptions in these models are 20+% down, the use of a negative amortization loan, and rapidly climbing rental rates…all very aggressive, risky assumptions. As the economics of the past few years have borne out, this was a massively faulty model, relying on pie-in-the-sky fundamental assumptions.

I decided to move forward with the East Texas investment model. We bought our first house in March, 2003, and quickly built up a portfolio of 50 properties, mostly single family homes and a couple of duplexes. The total amount of rentals is 60. We established local banking relationships and negotiated portfolio loans that would lend to our limited partnership. We have an internal staff that manages and maintains the properties, and the cashflow from the properties more than covers all our expenses and the paydown on the principal.

It was interesting to go through the housing crisis with this portfolio, because this is where the initial fundamentals of the model were put to their test. As it turns out, because the fundamental values of the homes were not out-of-whack to begin with, the median home prices remained steady throughout the housing crisis. The community continues to grow, and rental rates and occupancy continue to be strong.

As a side note, we weren’t fully scaled up around our property management and maintenance infrastructure because I felt that I wanted our internal costs to be less than if we hired an outside property management company. It was a couple of years ago, and I didn’t want to add to the portfolio because of the massive instability in the housing market and the fact that many of the banks were scared to lend. We looked at our capabilities and decided to start a heating and air conditioning company in the area, leveraging off the infrastructure we built to manage and maintain the property portfolio. The HVAC company is doing very well with minimal management focus, thanks to an interesting business model that is very different than the other related companies in the area. This has been an exciting venture which has increased the profit of our property portfolio because of the shared overhead costs. Now we’re fully scaled over our infrastructure.

I look back on the bullet I dodged by not investing with the crowd, and I feel very fortunate that I stuck with the fundamental principals upon which I started.

My major takeaways from this experience are 1) you can find a good investment even during a bad time to invest, 2) build a good conservative financial model, and; 3) ALWAYS stick to the fundamentals!

I’d love to hear other lessons learned while riding out the real estate crisis…

Cheers,

Brian Royston

Royston Financial Consulting, Inc.

Monday, July 12, 2010

What's with the name?

Why the name Underpants Finance?

I provide financial consulting and modeling to growth companies in the San Francisco Bay Area. One of my social media savvy friends, Dave Nielsen, told me I should start a blog. After he convinced me to do so, I asked him what he thought I should call it. Dave thought for a while and then said, "Do you remember the Southpark episode with the Underpants Gnomes?" I had a vague recollection of the episode which came into greater focus as he explained it...

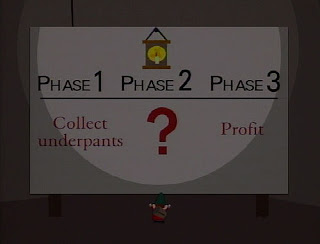

Underpants Gnomes were stealing one of the Southpark kids' underpants out of his dresser late at night. When the kids finally cornered one of the gnomes, the gnome took the kids to their lair and basically gave them a one slide Powerpoint presentation of their business plan, shown below:

Phase 1: Collect underpants

Phase 2: ?

Phase 3: Profit

Dave said, "That's what you do! The Underpants Gnomes need you to help them with Phase 2!" We laughed, and the Underpants Finance blog was born.

I came home and did some research. Per Wikipedia, the underpants gnomes and, particularly, the business plan lacking a second stage between "Collect underpants" and "Profit", became widely used by many journalists and business critics as a metaphor for failed, internet bubble-era business plans. Motley Fool referenced the episode in 2001, Businessweek referenced it in 2007. Six months ago, Paul Krugman evoked the Underpants Gnomes in a rant about the pending health care bill. There's a book on Southpark philosophy which discusses the Underpants Gnomes. These gnomes are everywhere. They're even in academia: Paul Cantor, a literary and economic professor who uses South Park episodes to teach courses, said "no episode of South Park I have taught has raised as much raw passion, indignation, and hostility among students as 'Gnomes' has."

Later that day I was on a bike ride, thinking about a financial model I was building for a client. I thought how funny it would be to rename my company Underpants Finance...or even better...Underpants Modeling. I laughed to myself and sent a text to Dave about the name Underpants Modeling. He shot back, saying, "I can just hear you tell someone...I will make you an 'underpants model' ;-)"

Anyway...that's where the name came from...bizarre, huh?

There are a lot of companies out there that have a great vision and a strong grasp of their market. What they're lacking is a detailed financial model. A detailed financial model takes the leadership's vision and translates it into an executable plan, with budgets, benchmarks and milestones that are measurable and actionable. It builds a bridge between vision and execution, and details how the resources (cash, personnel, capital equipment) will be used in getting from Phase 1 to Phase 3.

So that's what I'm going to focus on from now on...financial models to help you sell your underpants. So let me know if you want me to make you an Underpants Model!

;-)

Brian Royston

Chief Underpants Modeler

Royston Financial Consulting, Inc.

I provide financial consulting and modeling to growth companies in the San Francisco Bay Area. One of my social media savvy friends, Dave Nielsen, told me I should start a blog. After he convinced me to do so, I asked him what he thought I should call it. Dave thought for a while and then said, "Do you remember the Southpark episode with the Underpants Gnomes?" I had a vague recollection of the episode which came into greater focus as he explained it...

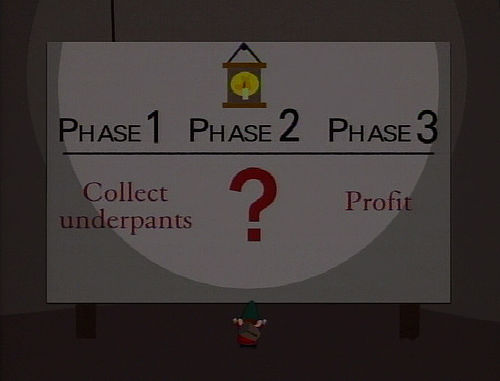

Underpants Gnomes were stealing one of the Southpark kids' underpants out of his dresser late at night. When the kids finally cornered one of the gnomes, the gnome took the kids to their lair and basically gave them a one slide Powerpoint presentation of their business plan, shown below:

Phase 1: Collect underpants

Phase 2: ?

Phase 3: Profit

Dave said, "That's what you do! The Underpants Gnomes need you to help them with Phase 2!" We laughed, and the Underpants Finance blog was born.

I came home and did some research. Per Wikipedia, the underpants gnomes and, particularly, the business plan lacking a second stage between "Collect underpants" and "Profit", became widely used by many journalists and business critics as a metaphor for failed, internet bubble-era business plans. Motley Fool referenced the episode in 2001, Businessweek referenced it in 2007. Six months ago, Paul Krugman evoked the Underpants Gnomes in a rant about the pending health care bill. There's a book on Southpark philosophy which discusses the Underpants Gnomes. These gnomes are everywhere. They're even in academia: Paul Cantor, a literary and economic professor who uses South Park episodes to teach courses, said "no episode of South Park I have taught has raised as much raw passion, indignation, and hostility among students as 'Gnomes' has."

Later that day I was on a bike ride, thinking about a financial model I was building for a client. I thought how funny it would be to rename my company Underpants Finance...or even better...Underpants Modeling. I laughed to myself and sent a text to Dave about the name Underpants Modeling. He shot back, saying, "I can just hear you tell someone...I will make you an 'underpants model' ;-)"

Anyway...that's where the name came from...bizarre, huh?

There are a lot of companies out there that have a great vision and a strong grasp of their market. What they're lacking is a detailed financial model. A detailed financial model takes the leadership's vision and translates it into an executable plan, with budgets, benchmarks and milestones that are measurable and actionable. It builds a bridge between vision and execution, and details how the resources (cash, personnel, capital equipment) will be used in getting from Phase 1 to Phase 3.

So that's what I'm going to focus on from now on...financial models to help you sell your underpants. So let me know if you want me to make you an Underpants Model!

;-)

Brian Royston

Chief Underpants Modeler

Royston Financial Consulting, Inc.

Subscribe to:

Posts (Atom)